AI Agents for Fund Administrators: A Practical Adoption Guide

Which processes to automate first, the shadow-to-production promotion path, what FINMA and ESMA expect, and the questions to ask any agent vendor.

Fee pressure is structural and headcount is the cost base. A practical adoption path for fund administrators who want AI agents in production without risking client deliverables.

For a fund administrator, the realistic way to adopt AI agents is narrow and staged: pick one high-volume manual process, deploy an agent for it in shadow mode alongside the existing team, measure the error rate against human output, then promote it to production with human sign-off retained. Administrators that try to "transform operations with AI" as a program tend to stall in committees. The ones that automate statement ingestion for a single client fund in a quarter build from there.

Why administrators specifically

Fund administration is a per-seat business under per-basis-point pricing. Revenue scales with AUA while costs scale with headcount, and every new fund onboarded brings another set of broker formats, custodian portals, and reporting templates for the operations team to absorb. Meanwhile fee pressure from managers is constant, and the administrators winning mandates are the ones quoting faster NAV delivery at lower cost.

The adoption signal from the client side is already clear: Mercer's 2024 global manager survey found 91% of investment managers using or planning to use AI. Managers who run AI inside their own investment process will expect their administrator to keep pace on the operations side, and will notice when a competitor administrator closes NAVs in hours instead of days.

Which processes to automate first

Ranked by fit, based on volume, input variety, and how cleanly the output can be checked:

- Statement ingestion and transaction capture. The highest-volume, lowest-judgment work in the shop. An agent pulls statements from portals, inboxes, and blockchains, and converts every format into the layout your platform expects. This is where the hours are, and errors are caught by existing reconciliation controls downstream.

- NAV input preparation and checks. Loading structured data into Paxus, NTAS, or Geneva, running completeness and tolerance checks, and queueing exceptions. The engine still calculates; the accountant still signs. We covered this pipeline end to end in Automating NAV calculation with AI agents.

- Investor onboarding document processing. Extracting data from subscription documents and KYC files into the transfer agency system, with the compliance officer reviewing a pre-filled record instead of typing one.

- Reporting drafts. Investor statements, board packs, and regulatory filings drafted from live system data, reviewed by the team before release.

- Reconciliation narratives. Agents that investigate breaks, gather the supporting entries from both sides, and propose the explanation for a human to confirm.

Deliberately absent from this list: anything involving valuation judgment, final sign-off, or direct unreviewed communication to investors. Those stay human, both because judgment lives there and because your control framework, and your SOC report, say so.

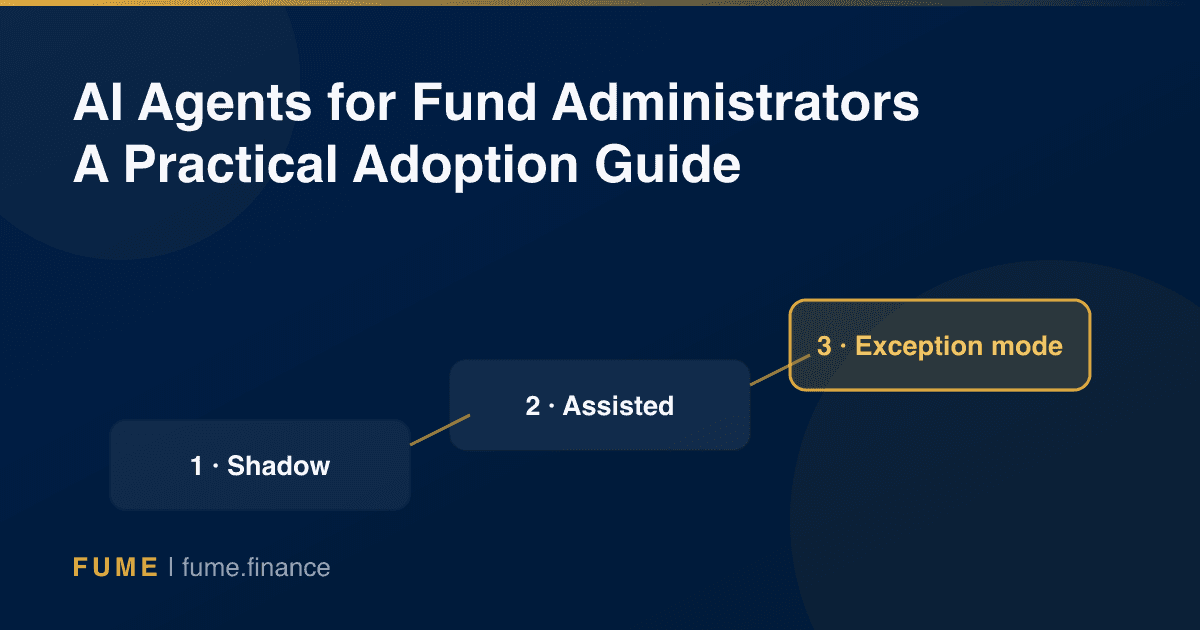

The three-stage promotion path

- Shadow mode. The agent runs in parallel with the existing process for two to four NAV cycles. Nobody relies on its output. You compare agent output to human output daily and measure the disagreement rate. This stage costs nothing in risk and produces the number your risk committee actually needs.

- Assisted mode. The agent's output becomes the working draft; a person approves every item before it posts. Throughput rises immediately because reviewing is faster than producing.

- Exception mode. The agent posts routine items inside defined tolerances on its own; humans handle only the exceptions it escalates. Most teams stabilize here, and it is the right place to stabilize. Full autonomy with no review queue is not the goal in a regulated deliverable.

What supervisors expect from you

Both of the frameworks most relevant to European and Swiss administrators are already published, and both are compatible with the staged path above.

FINMA Guidance 08/2024 expects supervised institutions to keep an inventory of AI applications, assign clear responsibility for each, manage model and data risks, and test and monitor continuously with fallback mechanisms in place. ESMA's May 2024 statement makes the same point under MiFID II: the firm remains responsible for outcomes, and record-keeping must document how AI is used, which data sources feed it, and what changed over time.

In practice this means each agent needs a named owner, a run log, documented limits, and a fallback ("the team does it manually") that you have actually rehearsed. None of this is exotic; it is the same discipline you already apply to any outsourced or automated control.

Build in-house or bring in a specialist

Large administrators with standing engineering teams can build on model APIs directly, and some will. For everyone else the honest math is that agent engineering is a full-time discipline: prompt and pipeline design, evaluation harnesses, monitoring, model updates, and the long tail of format edge cases. Hiring that team to automate one operations department rarely pays.

The alternative is a managed deployment: a specialist builds the agent around your exact process, wires it into the platforms you already run, and operates it, while your team reviews output through the same queues as before. That is the model we run at Fume with AI agents for funds, and it exists precisely so administrators do not need to become AI companies to get the outcome. Administrators who white-label Fume's tokenization engine get the same leverage on the onchain side: the agent chain and the tokenized register are built to work together.

Questions to ask any agent vendor

- Does the agent integrate with our existing platforms, or does it assume a migration?

- Can we run it in shadow mode against our team's output before relying on it?

- What does the run log contain, and can we hand it to an auditor as-is?

- What are the defined limits on autonomous action, and who sets them?

- Who monitors the agent day to day, and what is the fallback when it fails?

- What happens to our data, and where does it go?

A vendor with good answers to these six questions is offering you an operations capability. A vendor without them is offering you a demo.

For the broader context, what agents are, how they differ from the chatbots and RPA you have already tried, and where they fit across the whole fund lifecycle, our pillar guide covers AI agents for fund operations from first principles. If you would rather start from your own process list, book a call and we will go through it together.